Why The National Debt Matters

A response to Saurabh Sharma

Let me just start off by saying, I love Saurabh Sharma, Nick Solheim, and the good work they’re doing over at American Moment. Their take on so many of the relevant issues of our day tends to be on point more often than not, and certainly more often than a lot of the better-established conservative commentators.

They organized a few years back with the mission of finding a way to train and credential the rising generation of conservative staff and personnel in government, after seeing the Trump Administration spend so long struggling with incompetent or disloyal staff undermining the America First agenda at every turn. Clearly this is a much-needed project, and I definitely wish them all the success in the world at it.

And they also run a podcast. Called “Moment of Truth,” they interview a wide variety of people on a wide range of topics, some of them things that you don’t even hear commonly discussed by anyone. But I was a bit shocked on today’s episode (Feb. 13, 2023) to hear Saurabh admit that he didn’t really get what the whole deal was with the national debt.

18:04: Saurabh: I will be entirely honest. When people start talking about the national debt, I start falling asleep. Why should I care?

Jeffrey Anderson: You know, that’s a good question. A lot of people seem to have that attitude. … Right now, for every nine dollars Americans send in in tax money, the first dollar or so basically just gets thrown in the trash. Federal government takes it and doesn’t spend it on anything, it just goes to interest payments on the debt. If you get forced to pay $9000 in federal income tax, the first thousand dollars is basically just wasted. … And the only reason it’s only that low is because we’ve had historically low interest rates for quite some time.

…

Jeffrey: To put it in perspective, when Ross Perot ran for President in 1992, and he managed to get 19% of the popular vote, mostly by talking about our out-of-control spending under George H. W. Bush … 19% of the vote is massive for a third-party candidate. Our debt at that time was $4 trillion. We’re now at $31 trillion, 30 years later.

…

Saurabh: But here’s the thing. There were fiscal conservatives and reformers that were raising just as much hell about the $4 trillion as they are today about the $30 trillion. And it’s not obvious to me that the catastrophization that they may have been making at $4 trillion actually came to pass.

Jeffrey: Well I think some of that’s the low interest rates. The percentage of Americans’ tax payments that goes basically into the trash, to pay for interest payments on the debt, hasn’t really risen a whole lot from back in that general Perot era because interest rates dropped so much. But that’s not a perpetual thing; it’s gonna get worse in that regard. Thomas Jefferson talked about how, in terms of things that lead to wretchedness and oppression, the Four Horsemen of the Apocalypse, the lead horse is debt.

Jeffrey makes a good point here, but he misses an even better one: the low interest rates are the forewarned catastrophization coming to pass. He explains that the low interest rates helped deal with the debt, but not that they were caused by it, and not how they’ve been causing harm to America ever since.

It’s the stupid economy

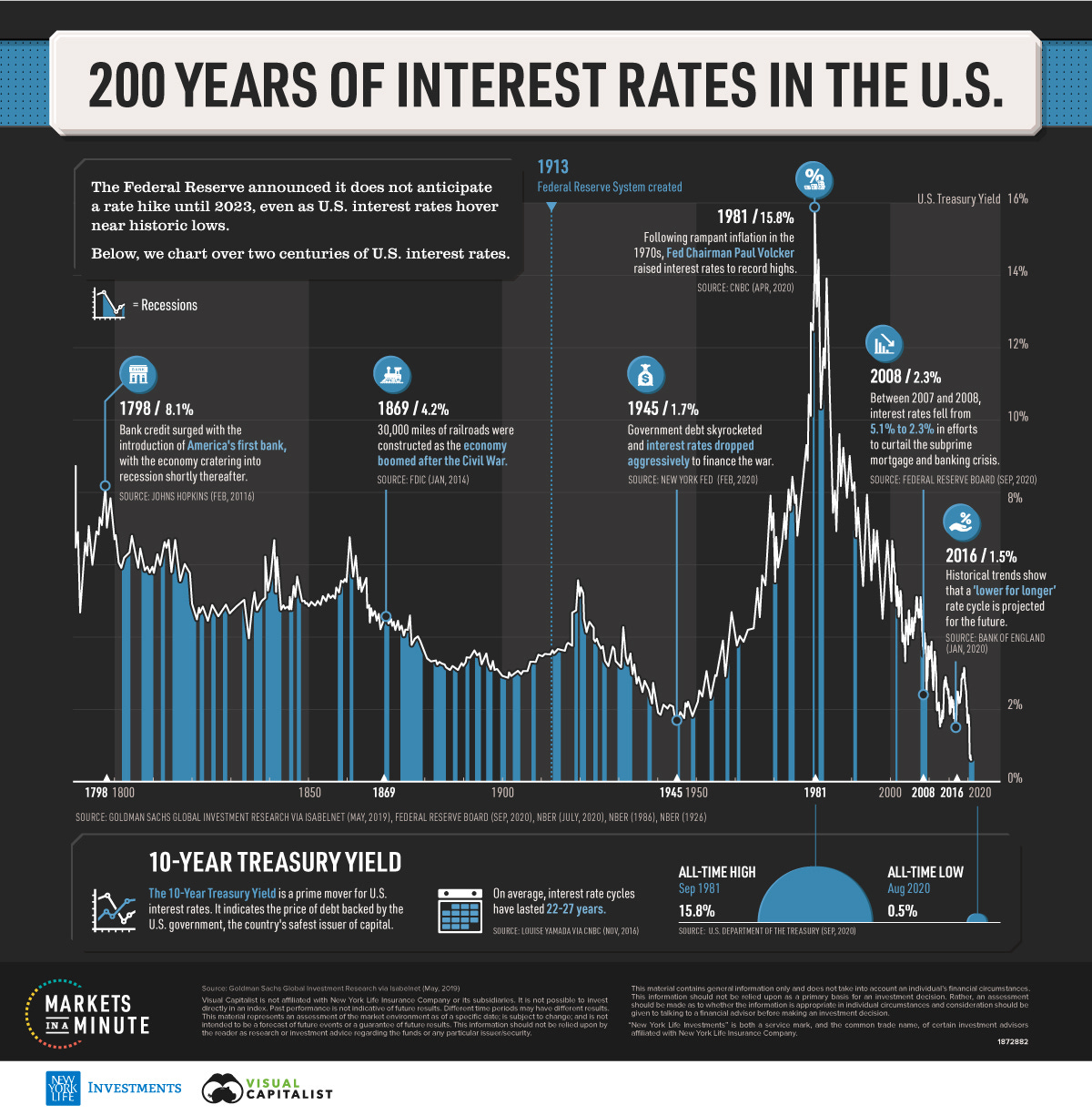

Have a look at this chart from Visual Capitalist showing the history of US interest rates over history. Things bounce around pretty wildly, but you kind of get the sense that the “comfort zone” is between 4-7%. When it goes much higher or lower than that, it’s a sign that things are going wrong. (The chart ends in 2020, so its predictions about future rate hikes are a bit out of date, but let’s look past that for the moment.)

In 1992, rates were still on their way back down, getting back to normal after the extreme measures that the Fed took in the 70s and early 80s to get inflation under control. I was in middle school back then, and it was a tremendously exciting time to have a bank account: I’d put my hard-earned allowance/chores money in, and every month I’d get a letter from them showing some real gains in the interest they paid out to me!

But rates just kept falling and falling. After 1992, Bill Clinton got elected, and falling interest rates made it much easier to get loans. The folks on the news told us the economy was booming, the invention of the World Wide Web led to big booms in technology companies, an embattled Clinton got re-elected by telling everyone to pay no attention to that scandal behind the curtain because “it’s the economy, stupid!” I was in high school by this point and I recall thinking, as the years went by, “if the economy’s so awesome, why is it so hard for my parents to find work? Why do I have more money sitting in my savings account but I’m earning less interest on it? Why can I not afford to take the girls I like out on dates?” While the news and the politicians said everything was booming, it really felt like Main Street was in a perpetual recession during those years.

Well, then 2000 came around, and we found out a little of what had been going on: all that “booming” money in the economy had been going into shady “.com” stocks in the stock market, and when people woke up and realized that most of these businesses had no real business being in business, the whole thing blew up. Clinton’s “economy, stupid” turned out to have been a pretty stupid economy afterall, and it left a lot of people feeling pretty stupid about it. But there were a lot of big-money investors who’d cashed out near the top, and they needed somewhere to put their money.

Money sitting around in cash doesn’t pay any interest, and when it’s parked in a bank account or Treasury bonds and rates are falling, falling, falling, that doesn’t pay very much interest either. So they started looking for something new to invest in, and settled on real estate. Well, we all know how that turned out! There’s a good case to be made for the idea that real estate is categorically the worst possible type of investment, but no one notices the downsides when the chart keeps going up. (When the money keeps rolling in, you don't ask how; think of all the people guaranteed a good time now!) With the help of Clinton-era policies coercing banks to make loans to unqualified buyers, (because if you don’t you’re raaaacist,) the free-flowing money pumped up a massive bubble in housing that caused significant harm to a lot of people who had thought “we’re homeowners now” once it burst in 2008. (The greatest harm of all, by far, was to low-income individuals and minorities, the very people these policies were supposed to help. This is a recurring theme with Leftist policies!)

George W. Bush had never been a particularly conservative President, but having this happen right at the end of his term tanked any possibility of getting a Republican to replace him, and so we got saddled with Barack Obama, and the government response to the 2008 crash was as far left as it gets: drown the problem in free money! Already-low interest rates cratered to essentially zero and the Federal Reserve went on a bubble-inflating spree. It was during the Obama years that we first heard the term “FAANG” as low-interest cash revived a brand new .com bubble. Meanwhile, just as housing prices were coming back down to sane levels after the bubble, a brand new bubble started to drive them back up just in time to price a significant portion of the rising generation of Millennials out of the market. It felt as if the Obama administration looked back on the biggest financial mistakes of the last two decades and said “yeah, let’s get us some more of that!” (This is another recurring theme of Leftist policies: they simply do not learn the lessons of history, even recent history.)

The sense of a schizophrenic economy that we first started to notice in the 90s came back with a vengeance in 2008 and has never really gotten better. With all the free money flowing, the news told us everything was awesome — and it sure was if you had a few million to invest in the stock market! — but most of the people who got laid off in the wake of the crash ended up taking new jobs at a 20-30% pay cut. Main Street stores have been closing down ever since. (Ever visit a “ghost mall”? I have.) With so many people priced out of the housing market, they’ve been forced into rentals, and so rental prices have skyrocketed. You could be forgiven for asking, throughout the Obama and Trump years, “if the economy is booming so much, why is it always such a constant struggle so much to make ends meet?”

Then COVID hit, and governments everywhere freaked out and imposed wildly destructive lockdowns. It was no longer possible to pretend the economy was booming, not with it grinding to a halt like that, so with a Leftist House of Representatives, a just-barely Republican majority in the Senate, a President getting poison whispered in his ears by Leftist bureaucrats, and Leftist media screaming toxic fearmongering at everyone at the top of their lungs, we ended up with massive stimulus checks getting passed, flooding the country with free money and driving inflation through the roof, and here we are today.

Incentives for inflation

Now, I can already hear you saying, “Bob, that’s all well and good, but what does any of that have to do with the national debt?”

Everything!

No, I’m serious; hear me out.

Imagine you had $1000, and then there was a sudden 10% inflation. You still have $1000, but now its purchasing power only feels like $900 to you. Everyone understands this. We just lived through it afterall.

Here’s the part so many people don’t understand: it works the same way on negative numbers. Instead of having $1000, let’s say you’re $1000 in debt, and then there’s a sudden 10% inflation. Now you’re still $1000 in debt, but the pain of it only feels like $900 to you. From the perspective of someone in debt, inflation doesn’t feel like such a bad thing.

From the perspective of a government trillions of dollars in debt, not only is it not a bad thing, it’s seen as a desirable policy goal. Look at where our money comes from: the Federal Reserve bank. One of the two mandates of the Federal Reserve is price stability. “Stable” is defined as “not changing or fluctuating” (adj. 1b) and “placed so as to resist forces tending to cause motion or change of motion” (adj. 3a(1)). So stable prices are prices that do not change, and when poked at, resist change and go back to normal quickly. Now look back at the Fed’s interpretation of price stability:

The Committee judges that inflation at the rate of 2 percent, as measured by the annual change in the Price Index for Personal Consumption Expenditures (PCE), is most consistent over the longer run with the Federal Reserve's statutory mandate.

We’ve seen a lot of well-understood words redefined over the last several years to mean things more convenient to Leftists, but did you know that “stability” was among them? This is straight-up 1984 territory: War is peace! Freedom is slavery! Constantly-increasing prices are stable!

Ever since the 1980s, interest rates have been in a persistent, long-term downtrend as a debt-management strategy, creating massive amounts of malinvestment, and when that malinvestment created crashes, the government used that as an excuse to drive interest rates to zero and start dropping helicopter money, first on the financial sector and then on the general public. Anything to create more inflation!

John Bull wading through the Fed’s bull

Remember the bit above, about Leftists not learning the lessons of history? We’ve known that low rates are a bad idea for a long, long time. In 1852, English economist Walter Bagehot wrote that “John Bull can stand many things, but he can’t stand [rates of] two per cent.”

People won’t take 2 per cent; they won’t bear a loss of income. Instead of that dreadful event, they invest their careful savings in something impossible – a canal to Kamchatka, a railway to Watchet, a plan for animating the Dead Sea, a corporation for shipping skates to the Torrid Zone. A century or two ago, the Dutch burgomasters, of all people in the world, invented the most imaginative occupation. They speculated in impossible tulips.

John Bull is a generic English name for the everyman, basically equivalent to the American “John Q. Citizen” or “Joe Sixpack.” Bagehot was explaining that, as interest rates fall too low, ordinary people (and particularly ordinary investors) are driven into crazier investments in search of yield, fueling speculative bubbles that then end in destructive crashes. And that’s been the story of American finance since the late 1990s. Internet businesses with no real business plan! House flipping! Fake digital money that’s never produced anything but crime and scams! The smallest notable American carmaker pumped to a higher market cap than all the rest of them put together! Stonks!

And all of it, the ongoing schizophrenic economy lurching from one disaster to the next, has been in pursuit of a low-rate, high-inflation agenda to keep the national debt manageable.

The benefit of history

A bit of quick Googling doesn’t turn up anything definitive about Saurabh Sharma’s age, but he looks fairly young. I did find his LinkedIn profile, though, which says that he went to college from 2015-2019. That suggests that he’s in his mid-to-late 20s today, and was born in the late 90s. (And he spent some amount of time in India before immigrating to the USA.) So his entire experience in the USA has been in the schizophrenic economy of the Clinton and post-Clinton period. He was probably still in middle school when the 2008 crash occurred.

To him, all of this feels normal. It’s the way things have always been, for as long as he’s been aware of conditions around him.

I don’t say this to disparage or belittle Saurabh, but simply to understand him and put this all in perspective. When something is “just the way things are,” it’s hard to feel like it’s a serious problem. But from the perspective of someone who was around before Clinton, we’ve been in a constant domino-push of alternating major disasters and minor slumps for over 30 years now.

We need interest rates to go back up to historical levels, and stay there long-term. They seem to have gotten spiked back up recently as a reaction to Bidenflation, but with debt this high, there’s no way it will be sustainable. Watch for the Fed to slash interest rates back down to insanity levels as soon as politically feasible. (Saurabh makes this point a few minutes further into the podcast.)

The only way to get our government out of the low-rates-high-inflation mindset is to get the debt under control. That means first balancing the budget, and then actually paying the debt down. It will take a while; we’ve been over $1 trillion for over 40 years now and, and just like all those pounds you’ve spent decades slowly packing on, that won’t go away quickly. It will take a real sense of national resolve, an understanding that debt causes financial insanity and inflation and we need to make it go away, and that understanding is just not there right now.

Conservatives urgently need to cultivate that understanding.

A modest proposal

Churchill famously predicted that America would always do the right thing, after exhausting every other alternative. Well, we’ve tried just about everything else for decades now, and debt keeps getting worse. How about we finally stop issuing more debt?

We can’t simply bring the bond auctions to an immediate halt, of course. We as a nation have been addicted to living beyond our means for so long that many people think it’s normal. “Addicted” is defined as “physically and mentally dependent on a particular substance, and unable to stop taking it without incurring adverse effects,” and that last bit is significant. Treatment of addiction is not just about getting someone to stop using, but about safely getting them out of the addicted state in which withdrawal will harm them. It often includes giving the addict other drugs that can help with the symptoms while keeping the intoxicating effects to a minimum.

The problem with bonds (our standard method of issuing government debt) is that, with durations measured in years or even decades, they separate the act from the negative consequences by long enough to severely blur the link between them in many people’s minds. This is why debt has been considered a moral failing throughout much of human history, and why the Law of Moses contained an absolute prohibition on long-term debt. No debt could last longer than 7 years, and every 50 years the entire slate was wiped clean in a society-wide jubilee. Why? To keep from ending in compounding debt traps like the one in which our nation currently finds itself.

But if we’re addicted to debt and don’t issue more debt, how will we keep from ending up in withdrawal?

By managing it with an alternative drug, that’s how. And here’s where I break with a lot of so-called “conservative" economists who are actually libertarians (aka. Leftists in sheep’s clothing): I believe we should sharply curtail if not entirely eliminate the issuance of new bonds, and replace it with monetization. If the government spends more than it taxes, fire up the Treasury’s printing press to make up the difference!

“But wait!” the libertarian wails. “That would cause massive inflation! No one wants that!”

To which I reply, “yes, that’s precisely the point.” If you take away the trickery used to kick the inflationary consequences decades down the road, and make the painful result happen right away instead of much later, no one will want that. I think we should move to a system of mandatory monetization because it’s the only thing that will get us to take debt seriously instead of making it our children’s problem. It would get people clamoring for Congress to take a hard look at where all that money is going and how much of it is really necessary.

“But, but, Weimar Germany!” the libertarian replies.

No, not at all. Weimar hyperinflation occurred as a result of attempts to use money-printing to pay off existing debts. But if we make a law that bonds may only be issued in an amount to cover X% of debt rollover for a year and no other reason, and X is a high value, (somewhere around 95%, for example,) then we’ve got a debt that’s slowly declining over the long term without dumping $30 trillion in inflation on the country all at once. This would give us space to get our financial house in order and focus on making the tough choices needed to get the deficit down to 0.

Then we can start to actually tackle the debt.

Then we can finally restore financial sanity in this country.

I’m not saying it will be easy, and I’m not saying it will be fast. But I’m saying it’s necessary, and in the long run it will be worth it.